“What do YOU think?” asked my client in an email regarding the recent op-ed by Robert Pozen in The Wall Street Journal titled, “You’re Probably Overinvested in Bonds.”

“He may be right,” I said. “But I think he’s wrong.”

The case Mr. Pozen makes is that stocks will outperform bonds and that the proper allocation is not the typical 60% in stocks and 40% bonds or a 60-40 portfolio, but rather, it should be 90% stocks and 10% bonds.

Sure, as Mr. Pozen explains, stocks have outperformed bonds over several time periods. But it’s the few major hits that have Your Survival Guy questioning his advice. Because I’ve been in the trenches with boots on the ground, fielding calls from retired investors during some of the worst markets this century. It’s not pretty.

I can tell you, from my unique perspective, that when times are tough, retirees do not care about “what stocks have done for the long-term or how they might recover.” What they care about is how much money they’re losing every day and how much longer it will go on for. They don’t have the luxury of time to “ride it out” when their spouse is asking them nightly, “How is our money doing?”

To be fair: “Plenty of people should hold bonds,” writes Mr. Pozen. “If you are retired and subsisting on your investment income, or if you would have to sell a significant chunk of your investments to cover living expenses in a bad year, you should have more in high quality bonds.”

I agree. But what about all those retirees who have IRAs that are required to take an RMD (required minimum distribution) and have 90% in stocks and the market crashes? The RMD is calculated on the prior year’s year-end balance, and the withdrawal amount may be a lot higher percentage of the account after the crash. It’s my belief that a more balanced portfolio, say 60-40, may help lessen the damage of a required distribution during a bad year for stocks.

I’ll also make the point here that $1 million isn’t what it used to be, especially with government in the business of inflation, creating more dollars to inflate away the debt. That $1 million will not go as far tomorrow as it does today. Which is why I believe investors need to be defensive in their portfolio allocations even if they have enough income coming in outside of it. Because there may be a time when the math changes and they’ll need to tap into their $1 million nest egg.

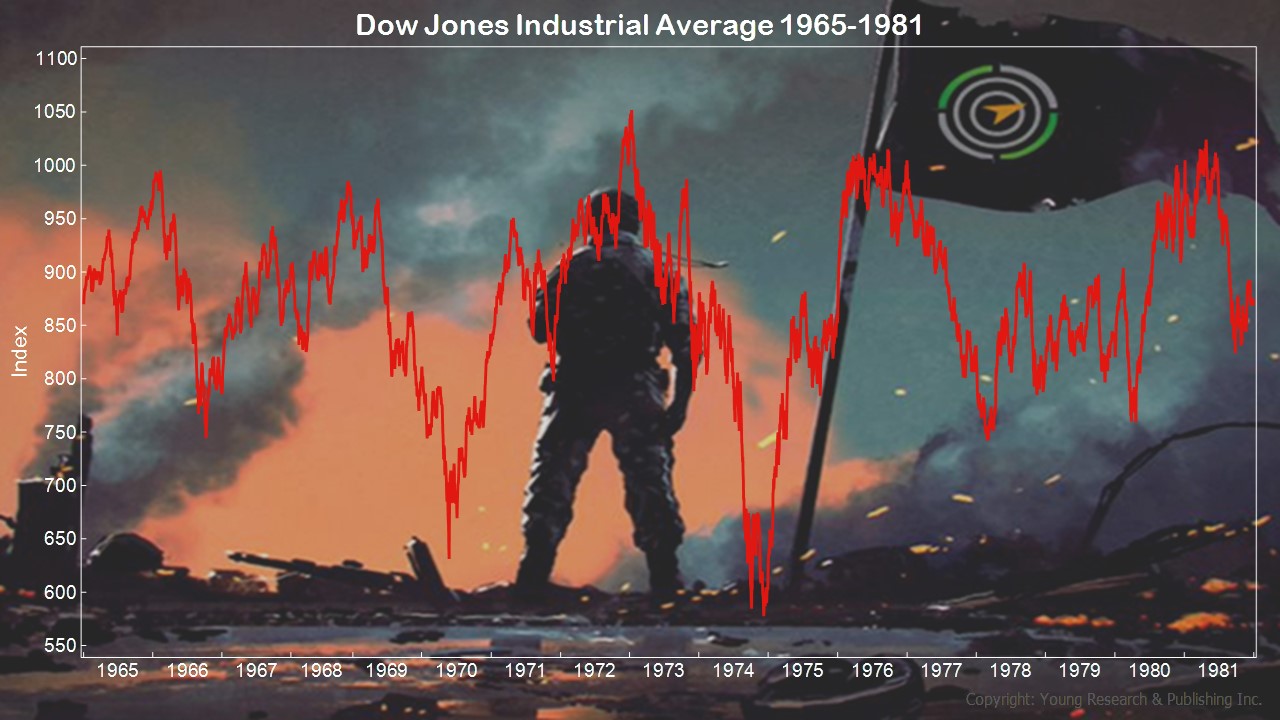

In reading House of Fidelity: The Rise of the Johnson Dynasty and the Company that Changes American Investing, by Justin Baer, you’ll learn how Mr. Pozen was hired as Fidelity’s general counsel, emerging as a key executive to Ned Johnson, during the 1990s. There’s a section in the book where, after the Go-Go 1960s, stocks went into a deep freeze. A time when Mr. Johnson needed to find ways to diversify the business, seeking other sources of revenue. When asked about this difficult time and what it was like, he remarks that he’s not sure he would have stayed in the business had he known it was going to last that long.

That doesn’t mean you load up on bonds. It just means you want to become a student of prices. As Ben Graham points out in The Intelligent Investor, you want to consider a 50-50 portfolio when stocks are richly priced, so you’re not making a prediction, and he suggests keeping within the parameters of 70-30 or 30-70 portfolio.

Action Line: Developing the right asset mix is more art than science. It’s more about understanding you. It’s not a one size fits all. When you want to talk about your situation, let’s talk. Email me at ejsmith@yoursurvivalguy.com.

Read more:

Originally posted on Your Survival Guy.